Some IT organisations prefer infrastructure solutions that offer simplified cloud deployment models for their digital transformation projects. According to the latest market study by International Data Corporation (IDC), worldwide converged systems market revenue increased 9.9 percent year-over-year to $3.5 billion during the second quarter of 2018 (2Q18).

"Data centre infrastructure convergence remains an important investment driver for companies around the world," said Sebastian Lagana, research manager at IDC. "HCI solutions helped to drive second-quarter market expansion thanks, in part, to their ability to reduce infrastructure complexity, promote consolidation, and allow IT teams to support an organisation's business objectives."

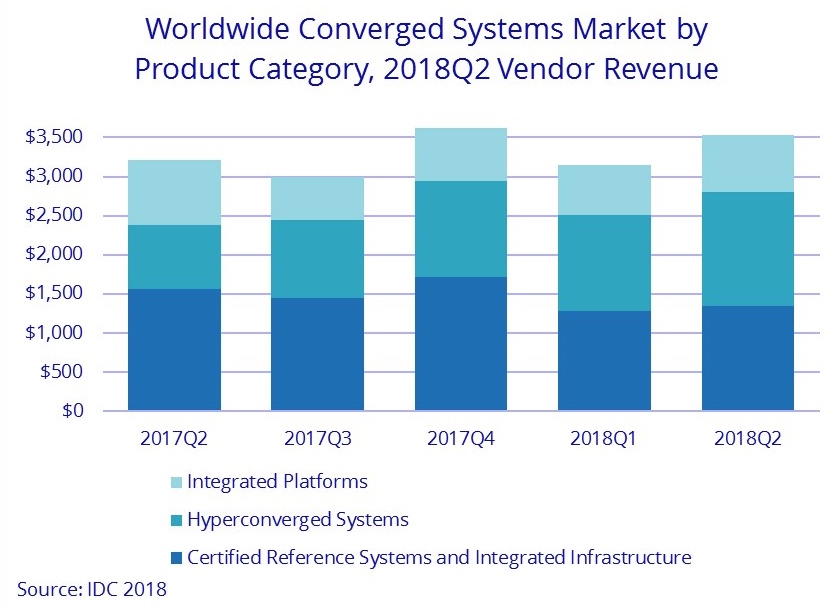

Converged systems market development

IDC's converged systems market view offers three segments: 1) certified reference systems & integrated infrastructure, 2) integrated platforms, and 3) hyperconverged systems.

The certified reference systems and integrated infrastructure market generated $1.3 billion in revenue during the second quarter, which was a year-over-year decline of 13.9 percent and represented 38.1 percent of total converged systems revenue.

Integrated platforms sales declined 12.5 percent year over year during the second quarter, generating revenues of $729.4 million. This amounted to 20.7 percent of the total converged systems market revenue.

Revenue from hyperconverged systems sales grew 78.1 percent year-over-year during the second quarter of 2018, generating $1.5 billion worth of sales. This amounted to 41.2 percent of the total converged systems market.

IDC offers two ways to rank technology suppliers within the hyperconverged systems market: by the brand of the hyperconverged solution or by the owner of the software providing the core hyperconverged capabilities.

Converged systems market segmentation

As it relates to the branded view of the hyperconverged systems market, Dell Inc. was the largest supplier with $418.7 million in revenue and a 28.8 percent share. Nutanix generated $275.3 million in branded revenue with the second largest share of 18.9 percent.

Cisco and HPE were statistically tied for the quarter, with $77.7 million and $72.0 million in revenue, or 5.3 percent and 4.9 percent in market share, respectively.

From the software ownership view of the market, systems running Nutanix's hyperconverged software represented $497.7 million in total second-quarter vendor revenue or 34.2 percent of the total market.

Systems running VMware's hyperconverged software represented $495.8 million in second quarter vendor revenue or 34.1 percent of the total market. Both amounts represent all software and hardware revenue, regardless of how it was ultimately branded.

Interested in hearing industry leaders discuss subjects like this and sharing their experiences and use-cases? Attend the Cyber Security & Cloud Expo World Series with upcoming events in Silicon Valley, London and Amsterdam to learn more.

Interested in hearing industry leaders discuss subjects like this and sharing their experiences and use-cases? Attend the Cyber Security & Cloud Expo World Series with upcoming events in Silicon Valley, London and Amsterdam to learn more.