The emergence of hyperscale cloud service providers transformed the enterprise computing environment. IT infrastructure vendors have learned to adapt to shifts in market demand and embrace the ongoing changes that have affected the data centre server and storage markets. Enterprise CIOs and CTOs have also modified their traditional budget allocations.

Total worldwide enterprise storage systems factory revenue was down 0.5 percent year-over-year, reaching $9.2 billion in the first quarter of 2017 (1Q17), according to the latest global market study by International Data Corporation (IDC).

Data centre storage market development

Total capacity shipments were up 41.4 percent year-over-year to 50.1 exabytes during the quarter. Revenue growth increased within the group of original design manufacturers (ODMs) that sell directly to hyperscale data center operators.

This portion of the market was up 78.2 percent year-over-year to $1.2 billion. In contrast, sales of server-based storage were down 13.7 percent during the quarter and accounted for $2.7 billion in revenue.

External storage systems remained the largest market segment, but the $5.2 billion in sales represented a modest decline of 2.8 percent year-over-year.

“The enterprise storage market closed out the first quarter relatively flat, yet adhered to a familiar pattern,” said Liz Conner, research manager at IDC.

According to the IDC assessment, spending on traditional external arrays continues to shrink, while spending on all-flash deployments once again posted strong growth and helped to drive the overall storage market. Meanwhile, the hyperscale data center business segment displayed solid growth in 1Q17.

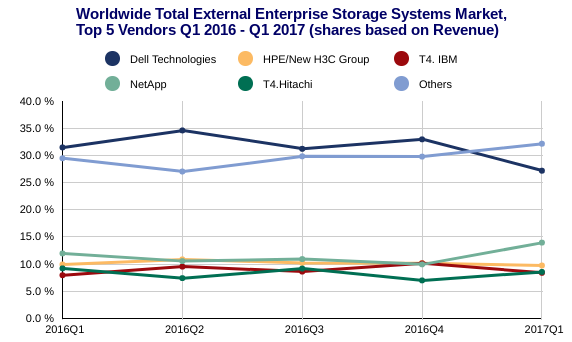

Dell held the top position within the total worldwide enterprise storage systems market, accounting for 21.5 percent of spending. HPE held the second position with a 20.3 percent share of revenue during the quarter.

HPE’s share and year-over-year growth rate includes revenues from the H3C joint venture in China that began in May of 2016. As a result, the reported HPE/New H3C Group combines storage revenue for both companies globally.

NetApp finished third with 8 percent market share. Hitachi and IBM finished in a statistical tie for the fourth position, each capturing 5 percent of global storage spending.

As a single group, storage systems sales by original design manufacturers (ODMs) selling directly to hyperscale datacenter customers accounted for 13.2 percent of global spending during the quarter.

The total All Flash Array (AFA) market generated almost $1.4 billion in revenue during the quarter, up 75.7 percent year-over-year. The Hybrid Flash Array (HFA) segment of the market continues to be a significant part of the overall market with $2 billion in revenue and 22 percent of the total market share.