Demand for computer servers, disk storage systems, and networking hardware deployed within an enterprise hybrid cloud environment remains strong. Moreover, the investment in non-cloud on-premises infrastructure seems assured by the CIO and CTO need to deliver superior security and compliance with IT regulatory requirements in several key industries.

According to the latest worldwide market study by International Data Corporation (IDC), vendor revenue from sales of IT infrastructure products for cloud environments — including public and private cloud — declined 10.2 percent year-over-year in the second quarter of 2019 (2Q19), reaching $14.1 billion.

Cloud IT infrastructure market development

IDC also lowered its forecast for total spending on cloud IT infrastructure in 2019 to $63.6 billion, down 4.9 percent from last quarter's forecast and changing from expected growth to a year-over-year decline of 2.1 percent.

Vendor revenue from hardware infrastructure sales to public cloud environments in 2Q19 was down 0.9 percent compared to the previous quarter (1Q19) and down 15.1 percent year over year to $9.4 billion.

This segment of the market continues to be highly impacted by demand from a handful of hyperscale cloud service providers, whose spending on IT infrastructure tends to have significant upward and downward swings. That ongoing fluctuation creates volatility for the IT infrastructure vendors.

After a strong performance in 2018, IDC expects the public cloud IT infrastructure segment to cool down in 2019 with spending reaching $42 billion — that's a 6.7 percent decrease from 2018. Although it will continue to account for most of the spending on cloud IT environments, its share will decrease from 69.4 percent in 2018 to 66.1 percent in 2019.

In contrast, spending on private cloud IT infrastructure has shown more stable growth since IDC started tracking sales of IT infrastructure products in various deployment environments. In the second quarter of 2019, vendor revenues from private cloud environments increased 1.5 percent year-over-year reaching $4.6 billion. IDC expects spending in this segment to grow 8.4 percent year-over-year in 2019.

Overall, the IT infrastructure industry is at crossroads in terms of product sales to cloud vs. traditional IT environments. In 3Q18, vendor revenues from cloud IT environments climbed over the 50 percent mark for the first time but fell below this important tipping point since then.

In 2Q19, cloud IT environments accounted for 48.4 percent of vendor revenues. For the full year 2019, spending on cloud IT infrastructure will remain just below the 50 percent mark at 49 percent.

Longer-term, however, IDC expects that spending on cloud IT infrastructure will grow steadily and will sustainably exceed the level of spending on traditional IT infrastructure in 2020 and beyond.

Spending on the three technology segments in cloud IT environments is forecast to deliver growth for Ethernet switches while computing platforms and storage platforms are expected to decline in 2019.

Ethernet switches are expected to grow at 13.1 percent, while spending on storage platforms will decline at 6.8 percent and compute platforms will decline by 2.4 percent. Compute will remain the largest category of spending on cloud IT infrastructure at $33.8 billion.

Sales of IT infrastructure products into traditional (non-cloud) IT environments declined 6.6 percent from a year ago in Q219. For the full year 2019, worldwide spending on traditional non-cloud IT infrastructure is expected to decline by 5.8 percent, as the technology refresh cycle driving market growth in 2018 is winding down this year.

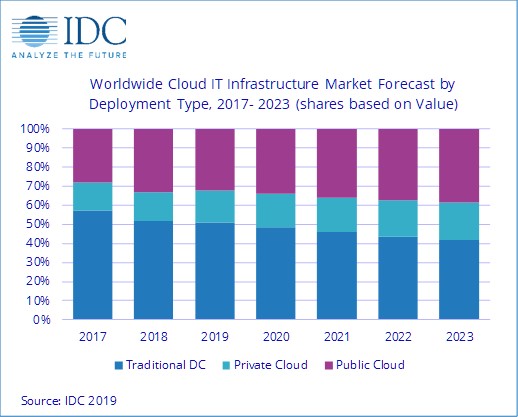

By 2023, IDC expects that traditional non-cloud IT infrastructure will only represent 41.8 percent of total worldwide IT infrastructure spending — that's down from 52 percent in 2018. This share loss and the growing share of cloud environments in overall spending on IT infrastructure is common across all regions.

Most regions grew their cloud IT Infrastructure revenues in 2Q19. Middle East & Africa was fastest growing at 29.3 percent year-over-year, followed by Canada at 15.6 percent year-over-year growth. Other growing regions in 2Q19 included Central & Eastern Europe (6.5 percent), Japan (5.9 percent), and Western Europe (3.1 percent).

Cloud IT infrastructure revenues were down slightly year-over-year in Asia-Pacific (excluding Japan) (APeJ) by 7.7 percent, Latin America by 14.2 percent, China by 6.9 percent, and the USA by 16.3 percent.

Outlook for cloud IT infrastructure investment

Long-term, IDC expects spending on cloud IT infrastructure to grow at a five-year compound annual growth rate (CAGR) of 6.9 percent, reaching $90.9 billion in 2023 and accounting for 58.2 percent of total IT infrastructure spend.

Public cloud data centres will account for 66 percent of this amount, growing at a 5.9 percent CAGR. Spending on private cloud infrastructure will grow at a CAGR of 9.2 percent.

Interested in hearing industry leaders discuss subjects like this and sharing their experiences and use-cases? Attend the Cyber Security & Cloud Expo World Series with upcoming events in Silicon Valley, London and Amsterdam to learn more.

Interested in hearing industry leaders discuss subjects like this and sharing their experiences and use-cases? Attend the Cyber Security & Cloud Expo World Series with upcoming events in Silicon Valley, London and Amsterdam to learn more.